First home buying: Part two

The New Zealand property market is no joke. In part two of our first home buying series, I explain how to figure out how much you could borrow, and look at some of the creative ways Kiwis are getting on the property ladder.

The current state of borrowing

With the recent increase in the OCR, we can expect mortgage interest rates to increase. This can mean banks reduce the amount they are willing to lend to borrowers. While this might reduce your potential purchase options and even put your dream home out of reach, all is not lost.

The dream home might just take a little while - or you might be surprised to find that your idea of the perfect home is more flexible than you thought.

We’ll share some inspirational ideas, but first, let’s figure out your borrow power to get your goals in motion.

How much can you borrow?

We created an easy mortgage borrow power calculator to estimate how much you could borrow.

All you have to do is enter your monthly income and expenses. The borrow power calculator then shows how much you could borrow and what your repayments would look like.

You can adjust parameters like how long it will take you to repay your mortgage. This is a great way to see how paying just a little extra each week can pay it off quicker and save you a lot of interest.

Of course, every lender has its own requirements so our calculator is an estimate only. Also, securing a home loan relies on having a deposit ready.

How much can you save for a deposit?

If you are eligible, you can use your KiwiSaver fund towards a deposit on your first home. Most home loans require a 20% deposit upfront. If it is your first home, you might qualify for a deposit as low as 5% via a First Home Loan.

Our KiwiSaver calculator will show you how much you could save in your KiwiSaver fund. You need to enter your income, when you plan to buy a home, your current KiwiSaver balance, contribution rate, and what type of fund you are in. Our KiwiSaver calculator then presents you with an estimate.

If the estimate is less than what you want, try seeing how much more you could save by switching your fund type or increasing your contributions.

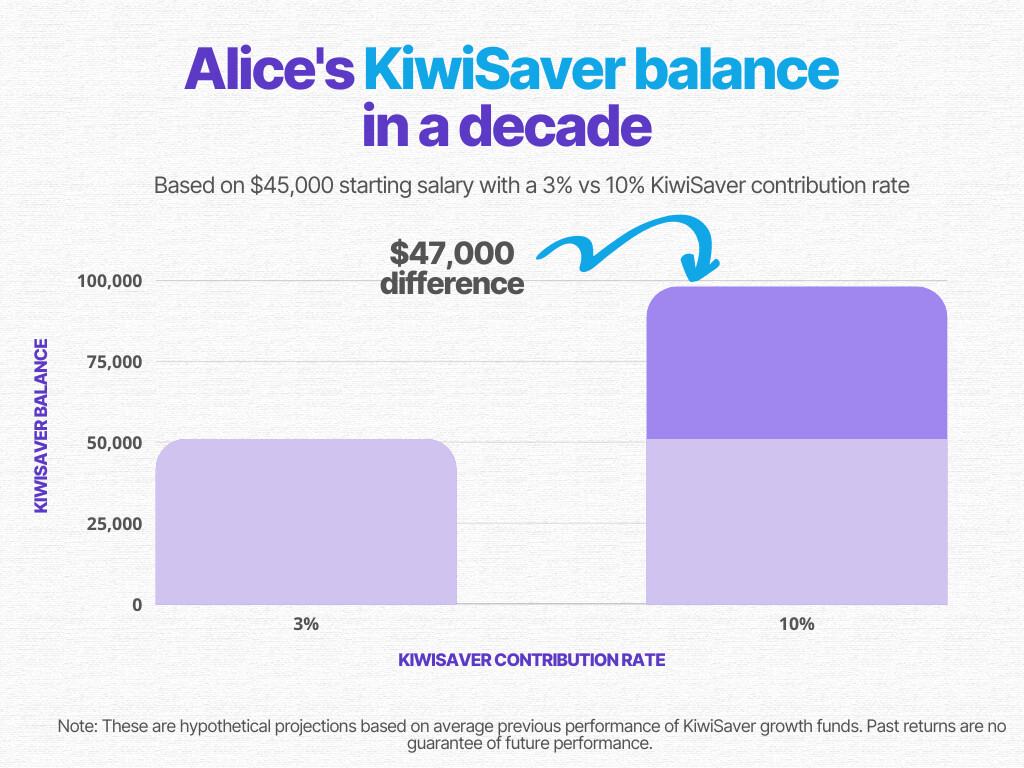

Here is an example: Alice is 25 years old and plans to buy a home in 10 years. She currently earns $45,000 annually before tax, her employer contributes 3%, and she has $5,000 in a Growth KiwiSaver fund. By contributing at the minimum rate of 3% of her wages, she could have $51,000 in 10 years. But if she increases her contribution rate to the maximum of 10%, she could have $98,000.

Get creative to get a home

Now you have an idea of how much you can borrow, it’s time to start looking around. If you can’t afford your dream home, settling for a more affordable option could get you on the property ladder and, in a few years, you could sell it to purchase what you really want. We found a few examples of outside-the-box thinking. Maybe you’ll find a little inspiration.

Homes under $325k in NZ? Yeah, right

If you are searching for an affordable mortgage, the regions could be your ticket.

At the time of this writing, you can buy a 3-bedroom home for as little as $250,000 - if you move to Westport.

It has its downsides. The West Coast gets a lot of spring rain and sometimes floods, at times cutting the area off from the rest of the country. And rural living is not for everyone.

But with the average home price of $325,000, more remote-working professionals are moving into the area. No commute, no traffic, just wild NZ landscape.

Commune with the parents

Parents own land? Buy a slice and stay close to home. Suffice to say you have to really get along with your family for this one to work.

A family in Horowhenua sub-divided their property and their daughter bought the section. Then she bought a prefabricated 92-square-metre house for $200,000. Now she lives next door to mum and dad. They share meals a few times a week and the dog gets double the treats.

Prefabricated homes are built off-site and then transferred to your section. It can be a bit trickier to get a mortgage, but not impossible. Usually, banks like for the home to be fixed to foundations to use it as security for a mortgage, but some banks have been flexible in recent years.

Not your granny’s flat

When you imagine buying a home, you likely think of a stand-alone structure that ticks all the boxes. But realtors say more and more young people are purchasing units, or what have sometimes been called ‘granny flats.’ These are usually bought by older people downsizing from a larger home, but now younger people are using units as a stepping stone.

For example, one realtor has a renovated unit in Christchurch on the market for $469,000 when the average stand-alone home in the same area is $750,000.

You get less space but also less maintenance. You’ll want to know if you’re buying a unit title or a cross lease and your rights and obligations. Some may restrict pets or whether you can make alterations to the unit. Like any other major purchase, do your research first.

Build… up?

Recently, a house in Grey Lynn, Auckland, sold for $300,000. It is a 9-square-metre shed that sits on 33 square metres. The family who purchased it will retain the historic shed and plan to build a 3-story home around and over it. (You gotta see it to believe it.)

In this instance, the property came with approved plans for the new build, so the owners knew they wouldn’t face any issues. Do your due diligence if you have big dreams for a quirky bit of land. Anything is possible - but you probably need consent.

Now what?

The borrow power calculator is a fast and easy way to gauge what you could potentially be eligible to borrow to buy a home. Talking to a financial adviser is the next step to ensure your estimates are realistic and you haven’t overlooked anything.

If you plan to use your KiwiSaver fund for a first home deposit, you must ensure that you are in the right fund. Which fund is best depends on your timeline, your risk tolerance, and how much you want to save.

The BetterSaver team has made it easy for you. There are over 250 funds out there and we have done all the research to match you to a better fund.

Take our fund finder quiz to find a better KiwiSaver fund in under five minutes.

The sooner you start saving, the closer you get to your dream home.